How Tamara Expanded Credit Access by 32% for the Modern Workforce with Financial Data

Tamara is Saudi Arabia’s homegrown FinTech platform, empowering millions of customers and thousands of merchants with innovative financial solutions. Founded in Riyadh, Tamara’s mission is clear: “We help people own their dreams”. Guided by this purpose, Tamara offers simple and flexible payments solutions, designed around how people manage their finances, inspiring greater control and confidence in their daily lives.

As Tamara scaled across the GCC, it identified a growing segment of modern workforce: gig economy workers, freelancers, students, and first-time digital finance users, who were eager to access credit, yet remained underserved by traditional frameworks. These systems typically relied on traditional data sources to track established borrowing and salary history. However, they were not designed to capture the real-time cash flow of the applicants with variable or non-traditional income.

Tamara saw an opportunity to strengthen its data visibility and gain deeper insight into the true financial health of credit worthy applicants. Addressing this gap would enable Tamara to responsibly extend credit to a modern, dynamic workforce. To do so, Tamara partnered with Lean to integrate verified financial data into its decisioning framework, unlocking a dynamic and complete view of income and affordability.

Challenges

While traditional data sources provided a baseline for credit checks, they offered partial insights into customer earnings. An analysis of thin-file customers revealed that a significant portion of people applying for credit had no salary information available in credit bureaus or through salary certificates.

Without verified income data, Tamara’s credit models remained conservative, leading to two main challenges:

1. Low credit limits

2. Application rejections for qualified applicants

The data gap was especially evident among customers with non-traditional income streams, including side businesses, commissions, marketplace activity, and investment earnings. Legacy records cannot capture these sources, but Open Banking data can provide real-time visibility and verified insights.

Solutions

Tamara and Lean approached the challenge with one guiding question: How do we better understand customers’ financial standing without adding friction or increasing risk?

Integrating Lean’s Open Banking data into Tamara’s credit decisioning framework created the missing layer of visibility. Real-time bank insights, paired with traditional data sources, revealed income patterns and financial activity that were previously out of reach.

With this, Tamara could assess affordability with far greater precision and confidence.

Through Lean, Tamara gained consent-based access to:

• Verified income directly from bank transactions

• Actual cash flow and spending patterns

• Existing financial commitments

• A clearer & more complete picture of customer affordability

This new visibility made it clear that many of the customers Tamara fetched did not receive a salary. Instead, they earned income from alternative sources that traditional datasets fail to capture. Lean’s income detection surfaced categories such as:

By incorporating a broader spectrum of income types, Tamara was able to assess affordability with far greater precision and include customers who had previously been invisible.

How Lean Helped Tamara Increase Approval Rates for Credit Limit Increases

Credit limit increases previously required months of customer activity before reassessment was possible. The visibility into real income and affordability became the foundation for a broader shift in how Tamara evaluated risk.

Enabling the Next Step: Second Look Lending

The new visibility into real income and affordability quickly became the basis for a broader shift in how Tamara evaluated risk. What began as a way to increase limits for existing customers evolved into a second look flow that allowed Tamara to revisit applications previously declined due to insufficient data. Many applicants weren’t risky, yet traditional sources offered no view into their true earning patterns, leaving valuable customers out of reach.

With Lean, Tamara introduced a streamlined second-look process:

1. Applicants declined due to missing data are invited to link their bank account through Lean.

2. Lean retrieves verified income and transaction history in seconds.

3. Tamara reasseses the application using real financial behavior rather than incomplete records

Results

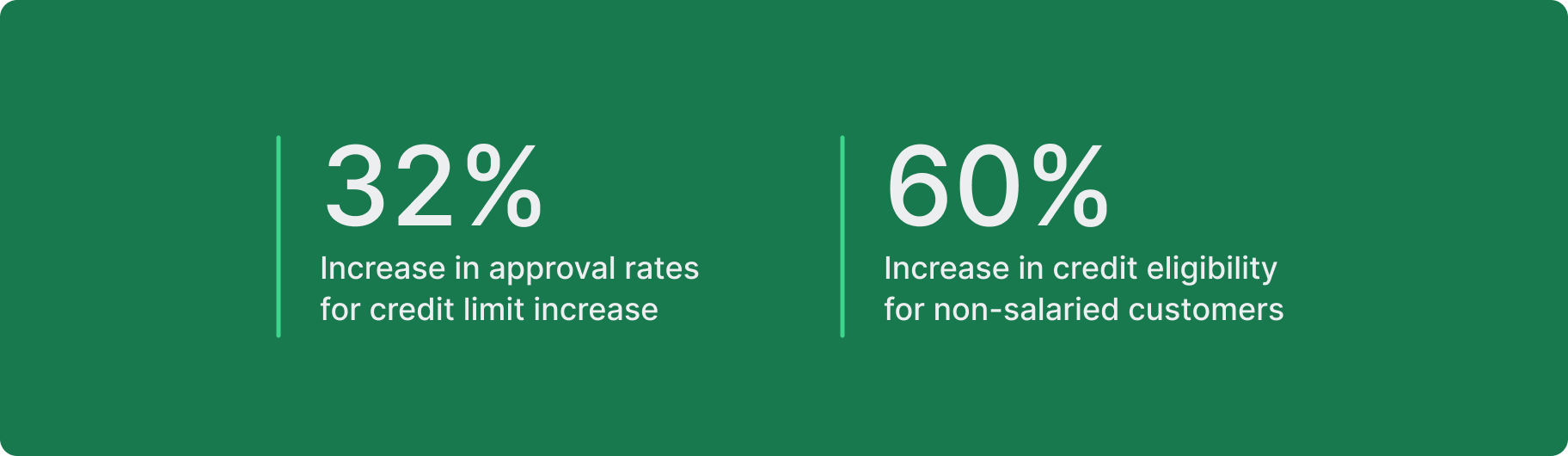

32% increase in approval rates

Bank-verified income improved for credit limit increases. This allowed Tamara to extend higher, more accurate credit limits to qualified customers and increase overall credit utilization without compromising risk controls.

60% more income visibility for non-salaried customers

Previously, Tamara found that a significant portion of applicants had no salary information available in traditional data sources. With verified financial data, Tamara can now see income signals for around 60% of these customers, enabling more accurate affordability assessments and extending fair credit to non-salaried applicants.

Tamara and Lean’s partnership shows what Open Banking can become when used to give lenders a deeper, more accurate understanding of their customers. This partnership expands access to responsible credit, improves the accuracy of decisioning, and strengthens trust between lenders and their customers. It’s a blueprint for how modern financial services should work: simple, data-backed, and built around real people.